Private Equity x Franchise Gyms

Exploring rolling up big-box franchise gyms as a private equity investment strategy

For those of you reading for the first time, welcome to Sweat Ventures. I write every other week on themes that catch my eye in the world of Fitness and Sports Investing.

Introduction

There are numerous strategies that private equity firms are pursuing to gain exposure to the explosive post-pandemic growth of the fitness industry. Over 60% of the top 20 gym chains in the US are now backed by private equity. One strategy I’ve increasingly seen is the consolidation of “big box,” value-oriented franchise gyms. More than 300 fitness franchise brands have been acquired by private equity firms since 2019. It’s important to note that I’m not referring to the acquisition of the franchisor itself but rather the process of rolling up the underlying franchisees.

In this post, I touch on the fitness industry tailwinds that have attracted institutional investors, give my take on the rationale and investment thesis behind this strategy, and quickly explore some representative transactions and key players.

Industry Tailwinds

The global fitness industry is valued at $257B in 2024 and growing at a 5.6% CAGR. This industry growth is driven by the adoption of digital fitness solutions and a shift in consumer interest towards fitness and wellness, accelerated by the COVID-19 Pandemic. Gym membership in the US has grown from 64.2M in 2019 to 87.3M in 2024.

The shape of the fitness facility industry is that of a barbell (no pun intended), in which business models thrive at both ends of the spectrum, but there is a gap in the mid-tier offerings. Luxury, high-end gyms focused on personalization, holistic health, and integrated wellness offerings target consumers with significant disposable income that they allocate to personal fitness.

On the other side of the barbell are the budget-friendly value offerings, which target consumers who want to pay a lower price for access to the basics. This is where we see franchised big box gyms with companies such as Planet Fitness, Anytime Fitness, Crunch Fitness, and Golds Gym.

I’ve been observing increasing activity in the market of private equity-backed groups rolling up and consolidating franchisees under these branded offerings. Aside from the industry growth, what features of these franchised gyms make them an enticing investment?

Investment Thesis

At the core of the thesis is fitness facilities have historically been a fragmented market, with the industry dominated by single owner/operators. This makes the acquisition targets relatively inexpensive and allows cash-rich private equity groups to roll up multiple add-ons while using little leverage. Beyond fragmentation, some additional considerations include:

Established Brands: Franchisees have established brand value, so there is less brand and marketing integration costs when consolidating multiple operations under one ownership group.

Bargaining Power: Consolidating under one franchisor banner tips the power dynamics back into the hands of the franchisee from the franchisor. A group with 100+ Planet Fitness’ in their portfolio will have more bargaining power with the franchisor compared to a single-unit operator.

Economies of Scale: Multiple units allow for bulk purchasing of equipment, apparel, technology, and third-party services, improving the margin profile across a system. There is also shared corporate overhead.

Multiple Arbitrage: As with any roll-up strategy, 1+1 sometimes equals 3. The larger the entity, the higher the multiple of EBITDA a future acquirer will pay for the system.

Talent: Acquiring multiple units provides access to a wider group of experienced and talented operators who can share their expertise and best practices across the entire system.

Real Estate: If the target franchisee owns the real estate as well, sale-leasebacks can free up additional capital to expedite expansion.

Diversification: Although this particular strategy doesn’t offer any brand or industry diversification, it can de-risk the platform from a geographic diversification standpoint, opening up exit opportunities and creating a more favorable business for lenders.

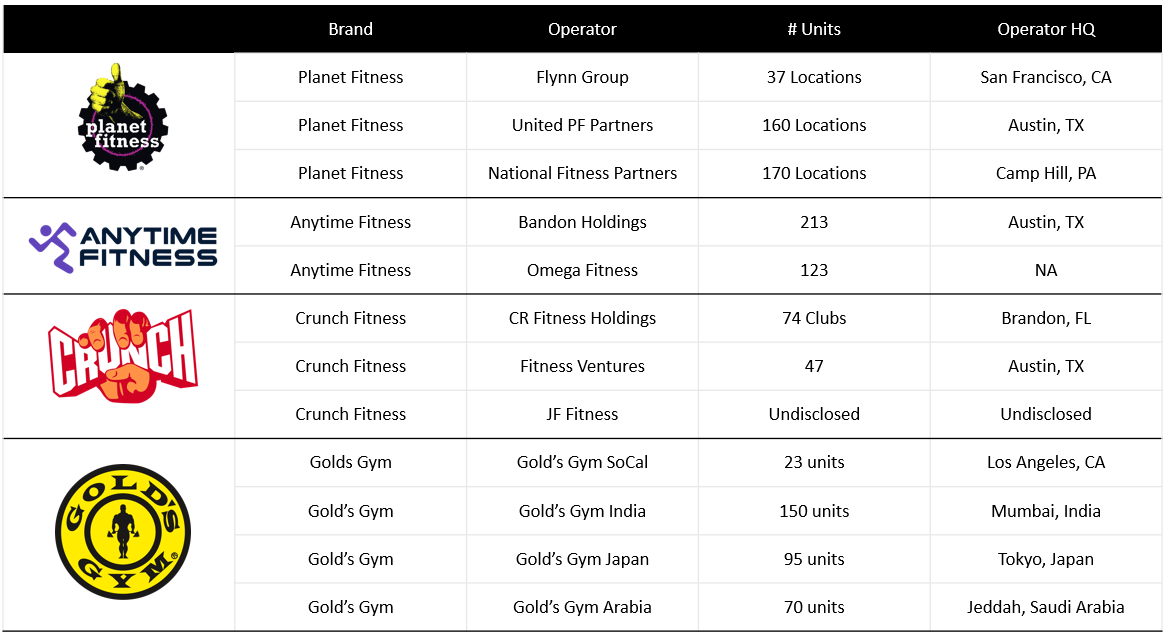

Below, I have highlighted some of the most active participants and detailed some representative transactions.

Key Players and Recent Transactions

September 2024: Omega Fitness, an Anytime Fitness franchisee backed by Rainier Partners, acquired 21 Anytime Fitness locations from MDS Fitness. This grew their portfolio of Anytime Fitness locations to 120 across California, Florida, Illinois, Minnesota, and Wisconsin.

July 2022: Sentinel Capital Partners acquired Austin, TX-based Bandon Holdings, the largest Anytime Fitness franchisee. Bandon operated 213 Anytime Fitness locations across 24 states.

April 2022: Olympus Partners acquired Excel Fitness Holdings, a Planet Fitness franchisee with over 90 units in operation, for over $675M.

November 2021: HGGC, a middle market private equity firm, completed a majority investment in PF Atlantic Holdings. At the time of the investment, PF Atlantic Holdings operated 42 Planet Fitness Locations.

June 2024: Primetime Fitness, a Crunch Fitness franchisee, completed the acquisition of 10 Crunch Fitness gyms across the US from Fitness Gurus.

August 2024: Meaningful Partners acquired Fitness Ventures LLC, the second-largest Crunch Fitness franchisee. At the time of the acquisition, Fitness Ventures LLC operated 47 Crunch Fitnesses in 25 states.

Below are a few larger franchise gym operators who have successfully consolidated in the space.

Potential Risks and Challenges

This strategy is not without risk. Below are some of the key threats that consolidators face:

Franchisor Governance: Despite having more power from the franchisee seat, consolidators are still subject to the fees and corporate decisions made at the franchisor level. Fees by brand vary but generally average ~7% of revenue as a royalty payment + 2% for a marketing fee. Decisions at the franchisor level are out of a consolidator's control and can dramatically affect operations.

Membership Attrition: Gyms on both sides of the barbell have historically had high membership attrition rates (30-50%). “Quitting day”, normally the 2nd Friday of January, is when many people give up on New Year’s resolutions, which often entail going to the gym more or using a gym membership. 80% of new gym members quit within the first five months of their membership. Retention strategies need to be a key focus for consolidators in the franchise gym space. One benefit of working with the lower cost, value offering, is there are often “sleeping members” who continue to pay for their gym membership without actually attending. This is more likely in situations in which the gym membership is not a significant part of a consumer's total discretionary income.

Changing Consumer Tastes: A final risk to the gym industry at large is the ephemeral nature of fitness trends due to changing consumer tastes and stiff competition. Gym operators that have a clear value proposition, whether that be a low price point or a differentiated offering, benefit by having some insulation against the “flavor of the month” dynamic in the fitness industry.

Key Takeaways

As consolidation continues and consolidators buy other consolidators, what was once a fragmented market will become concentrated in a few hands. As the big box brand opportunities run dry, I expect to see a similar strategy followed in the smaller and even more fragmented market, boutique fitness studios.

I hope this post helped you understand one specific strategy that private equity is pursuing within the fitness industry. In the next post, I’ll explore the related but distinct strategy of acquiring unrelated brands in a holding company structure. Thanks, as always, for reading.

.