Deep Dive on the NWSL

Investment considerations behind the explosive growth of the National Women's Soccer League

For those of you reading for the first time, welcome to Sweat Ventures! I write every other week on themes that catch my eye in the world of Fitness and Sports Investing. Thanks for joining!

Introduction

It's felt like almost every week in 2024, I've opened my e-mail to find a new piece of breaking news regarding the National Women's Soccer League (NWSL). Whether it's an announcement about a new expansion franchise, a change in ownership group, a new media deal, or a record-setting player contract, a lot is happening in this emerging sports property. Fueled by the tailwinds of a growing interest in women's sports at both the collegiate and professional ranks, the NWSL has become an active investment target within the sports asset class. I wanted to take a moment to explore the league, discuss my take on team valuations, and present both a bull and a bear perspective on the investment potential. Let’s dive in.

League History

The NWSL was created in 2012 as the female Major League Soccer (MLS) equivalent, a top-tier domestic soccer league that could compete with European counterparts. They weren’t the first with this mission and were preceded by failed leagues such as the Women's Professional Soccer League (2007-2012) and the Women's United Soccer Association (2001-2003). Previous leagues had been unable to grow or support operations over an extended period of time, ultimately leading to their demise. To create a more economically sustainable model, US Soccer, the Canadian Soccer Association, and the Mexican Football Federation agreed to subsidize team costs by paying the salaries of their national team players who played in the NWSL. Players on these three countries' national teams were distributed evenly across the league, creating a much smaller salary lift for team owners to field a team.

The subsidization efforts and the unification of predecessor league operators led the NWSL to be the first women's professional soccer league to last more than three seasons in the US. In March of this year they kicked off their 11th season, which will run to November. Of the 14 teams playing in 2024, three have affiliations with MLS teams (Houston Dash, Orlando Pride, and the Utah Royals) two teams have USL Championship affiliates (North Carolina Courage and Racing Louisville FC) and the remaining clubs are independently owned and operated (Angel City FC, Kansas City Current, NY/NJ Gotham FC, Portland Thorns, Seattle OL Reign, San Diego Wave, Chicago Red Stars, Washington Spirit, and Bay FC).

Growing Interest in Women’s Sports

Before diving into the specific investment considerations with the NWSL, it's important to note the significant growing interest in women's sports in general, both from a consumer and investor perspective.

This is a crucial tailwind lifting all NWSL franchise valuations. Since Congress ratified Title IX in 1972, women's sports have never been in a better spot as we enter 2024. Deloitte estimates that women's sports will generate $1B+ in global revenue this year, a 300% increase over 2021, and this growth is occurring across multiple sports.

The 2023 Women's World Cup in Australia/New Zealand had a global audience of approximately 2 billion after setting a previous high watermark of 1.12 billion in France in 2019.

There will be two professional women’s volleyball leagues that begin operations in 2024 (League One Volleyball and Pro Volleyball Federation: See Sweat Ventures post: 2024, The Year of Volleyball)

And finally, the growing interest in women’s sports is probably most pronounced in basketball. At the collegiate level, NCAA women's basketball is seemingly setting records on a nightly basis, primarily fueled by household names Caitlin Clark, Angel Reese, and Paige Bueckers. The 2023 Iowa-LSU title game drew 9.9M TV viewers, 2X the prior year, and not significantly far away from the 14.7M the men's title game drew between UConn and San Diego State. Depending on the matchup, some, including myself, believe this year's female title game has the potential to outrank the men. (Update: the Elite Eight Game between Iowa and LSU on April 1, 2024, drew 12.3M viewers, the most in women’s college basketball history).

As further evidence of the media interest, on January 4, 2024, ESPN announced a new eight-year media agreement with the NCAA, which includes the rights to 40 NCAA Championships (21 women's and 19 men's) and is valued at $115M annually ($920M contract value). The NCAA women's tournament was the crown jewel in this agreement and was initially projected to be spun out as a separate media entity. The NCAA decided to keep it packaged with the other properties but still comprises 56% of the deal's annual value, at ~$65M annually.

There is hope that the trajectory of women’s basketball at the collegiate ranks will carry over to the WNBA. Cathy Engelbert, commissioner of the WNBA, projects a $100M yearly deal after the current media deal expires with ESPN in 2025.

NWSL

The NWSL is one of the other success stories of this women’s sports movement. The 2022 Championship game had record viewership, with a 915k audience and 32k in attendance. (2023 was down slightly with 817k viewers and 25k in attendance). On November 9, 2023, the NWSL announced a new four-year $240M ($60M per year) media rights agreement with CBS Sports, ESPN, Prime Video, and Scripps Sports. All games not broadcast nationally will be accessible on the new internal streaming service NWSL+. The broadcast partners will also cover all of the production costs, which can run up to $80,000 per game or $10,000,000 per season. In the previous deal that burden fell on the NWSL.

This new four-year deal is 40x the previous $1.5M annual deal that the NWSL had with CBS, which was essentially a wash from a financial perspective after considering production costs.

With new media revenues buoying team valuations, ownership groups are investing in their talent from a retention and acquisition standpoint. This year, the league increased its salary cap by 40% to $2.75M.

In January 2024, the Chicago Red Stars signed Mallory Swanson to the richest deal in league history, five years, $2.5M total. This contract topped the Houston Dash's signing of Maria Sanchez to a three-year $1.5M deal.

Beyond shoring up existing talent, the NWSL is also getting more aggressive in the transfer market, looking to sign away Europe's top talent. Thus far, in 2024, there have been 21 inbound transfers to the NWSL compared to 6 during the same period last year. Total transfer fees in 2024 alone have exceeded $2M. Some notable transfers include Bay Area FC bringing Zambian striker Rachel Kundananji from Madrid CFF, Venezuelan Deyna Castellanos from Manchester City, and Nigerian forward Asosat Oshoala from Barcelona.

Beyond the media traction, the NWSL is also looking to capitalize on its merchandise opportunity. On March 11, they inked a deal with Amazon as the exclusive retail partner and official league licensee, which could create interesting synergies with fans watching the games and buying merchandise from Amazon.

Perhaps the most significant data point reflecting the NWSL growth is that earlier this month, the Kansas City Current played the inaugural match in CPKC Stadium, the first venue built explicitly for a professional women's sports team. The 11,500-person, $120M venue was almost entirely privately funded and sold out its first match in which the Current beat the Portland Thorns 5-4. Vahe Gregorian of the Kansas City Star said after the home opener:

"One small step for women certainly, one giant leap for womenkind. This already is a game-changer that has shifted the very dynamics of what is to be in the NWSL, where the impact on financial commitments has altered radically in the wake of the current's action."

Expansion franchise Boston FC might be the next team to make this leap into stadium ownership after they recently won a legal dispute, attempting to stop the renovation of White Stadium. The ownership group will put $50M into the renovation, and the city will contribute an additional $50M.

Stadium ownership by NWSL franchises not only shows a significant stamp of confidence by ownership groups in the league’s long-term potential but also drastically changes the economic profile of the sports team itself (more discussed below).

Recent Transactions

As I mentioned in the introduction, much of the news surrounding the NWSL has been due to multiple team transactions, including:

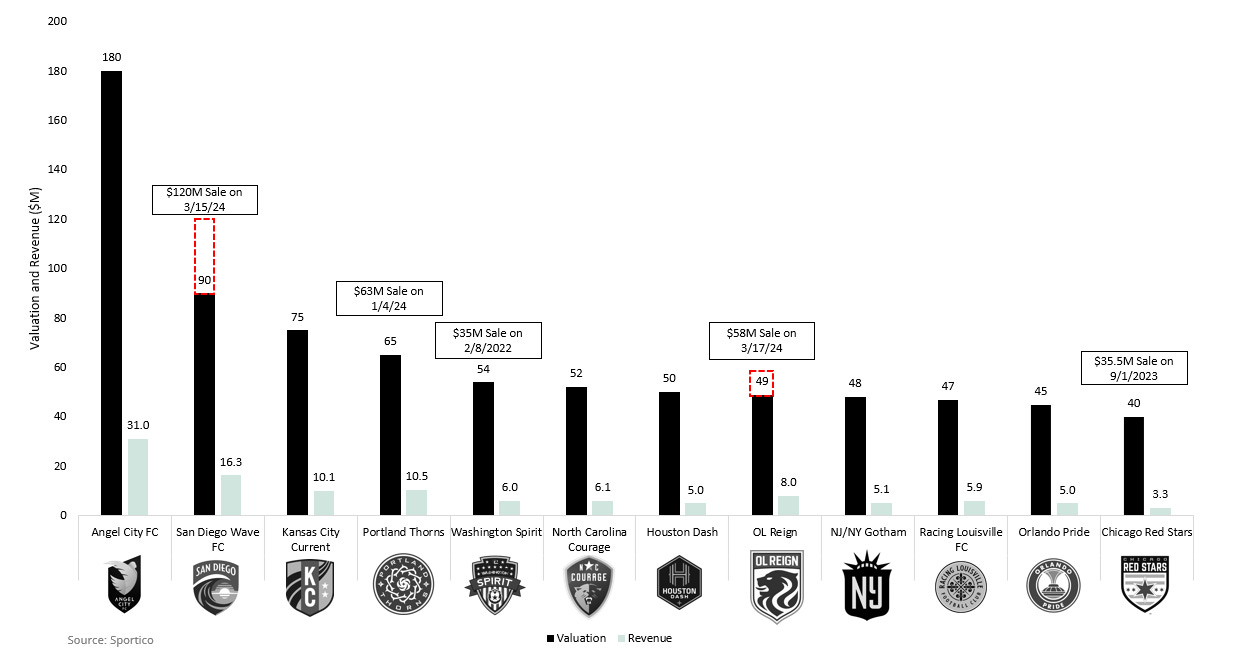

On March 15, 2024, Ron Burkle, former owner of the NHL's Pittsburgh Penguins, announced the sale of his ownership stake in the San Diego Wave to the Levine Leichtman family at a valuation of $113M. Lauren Leicthman and Arthur Levine, founders of Levine Leichtman Capital Partners, will pay $35M for a 35% stake in the team before the start of the season, with $78M paid at the end of the season for the remaining 65% at an appreciated valuation (weighted average valuation of $113M).

Burkle didn't state a specific reason for the sale but cashed in with a 56.5x return after paying just $2M as an expansion fee for the team in 2022. Note this doesn’t consider the additional capital that was most likely invested into the team to support operations.

Sportico, one of the most respected sources for sports team valuations, estimated a $90M valuation for the San Diego Wave on 2023 revenue of $16.3M, implying a 5.5x EV/TTM REV multiple. The actual transaction value implies that the Levine-Leichtmans paid closer to 6.9x TTM revenue.

The franchise has been successful with its ability to attract and build a fanbase. They had an attendance growth of 137.3% from 2022 to 2023, leading the league this past season with 20,718 per game.

On March 18 of this year, private equity firm Carlyle Group, in partnership with the MLS' Seattle Sounders, announced an acquisition of the Seattle OL Reign. The group bought 97% of the team from French firm OL Groupe at a valuation of $58M (Interestingly, former NBA Player Tony Parker owns the remaining 3%).

OL Groupe, acquired by John Textor's Eagle Football in December of 2022, bought the Reign in 2019 for $3M. The team has had consistently strong attendance, 4th in the league in 2023, with an average of 13,610 per game, 98.9% growth from 2022 levels.

Sportico estimated the Reign’s value to be $49M on $8M in revenue (6.1x). The $58M implies Carlye paid approximately 7.25x TTM revenue.

On September 1, 2023, a group backed by Laura Ricketts bought the Chicago Red Stars from Arnim Whisler at a $35.5M valuation, with a pledge to invest an additional $25M into the team and facilities. Ricketts, who also recently led a group to buy a 10% stake in the Chicago Sky (WNBA) at a $85M valuation, is part of the family that purchased the Chicago Cubs for $845M in 2009.

Whisler was facing pressure to sell the team after an investigation in 2022 revealed systemic issues of sexual misconduct and verbal abuse within the NWSL and the ownership group's failure to act on complaints. The Chicago Red Stars were among those teams listed in the report, specifically regarding former head coach Rory Dames.

Sportico listed the Red Stars as the NWSL’s least valuable franchise in 2023, with an estimated valuation of $40M on $3.3M in TTM revenue (12.1x). The team was last in the league in attendance at 4,884 per game, down 17.3% from 2022, despite having one of the biggest stars in the league, Mallory Swanson.

In January of this year, the Bhathal Family, investors in the Sacramento Kings (NBA), acquired the Portland Thorns from Peregrine Sports, controlled by Hank and Merrit Paulson, for $63M. The Bhathals will take over a club that ranked 4th in the NWSL in 2023 revenue, $10.5M, and third in average attendance, 18,918 per game (21.7% growth from 2022).

The previous owners of the Thorns were another group facing pressure to sell after being mentioned in the above-referenced investigation into systemic abuse within the NWSL.

Sportico estimated a 2023 value of $65M, representing a 6.2x multiple on 2023 revenue.

The most significant transaction in 2024 may be yet to come and would be the sale of a majority interest in Angel City FC. The most valuable club in the NWSL hired Moelis and Company to explore a control sale of the franchise earlier this year.

Angel City FC had $31M in revenue for 2023, which was top in the NWSL, and had the second-largest average attendance with 19,756 fans per game (a 3.4% increase from 2022). Sportico provided an estimated value of $180M, representing a 5.8x multiple on 2023 revenue.

Reasons for the potential sale are unclear, but many speculate infighting within the ownership group regarding governance and who actually controls the team. Angel City FC raised capital in an unorthodox way. Rather than having the backing of one foundational family office or PE group, they financed the team like a startup, raising a Series A round from a large group of individual investors. The team has three founding partners, Kara Nortman, Natalie Portman, and Julie Uhrman, and the largest shareholder, Alexis Ohanian, doesn’t control the board.

The process is still early, and details murky, but potential acquirers include Marc Lasry, former owner of the Milwaukee Bucks and current Managing Partner of Avenue Capital, a sport-specific investment fund.

Expansion

The league has also recently announced two new expansion franchises, another potential expansion in 2025, and the revitalization of one defunct franchise.

Bay FC, backed by private equity firm Sixth Street, is one of the new expansion franchises that began play in 2024. NWSL Boston is the other club recently granted expansion rights and will begin play during the 2026 season. Boston Unity Soccer Partners backs the team, an all-female ownership group led by Jennifer Epstein, Stephanie Connaughton, Ami Danoff, and Anna Palmer. The Boston and the Bay area franchises each paid a $53M expansion fee.

The NWSL also recently hired sports-focused investment bank Inner Circle Sports to explore the sale of a 16th franchise, which could fetch close to a $100M expansion fee.

The other new franchise that will begin playing in the 2024 season is the Utah Royals. David Blitzer, owner of MLS’ Real Salt Lake, and Ryan Smith, owner of the Utah Jazz will revive the Utah Royals franchise after the original Utah Royals moved to Kansas City in 2020. Due to previous agreements with the NWSL, the ownership group will be able to relaunch the franchise for a $2M expansion fee, which should give the team an immediate 26.5x markup in team valuation compared to the market rate for new teams.

Team Valuations

Given the appreciation of team values and the flurry of transaction activity, I want to take a moment to weigh my thoughts on the valuations of NWSL franchises. Before discussing the NWSL specifically, I will deviate slightly to provide some background on the business models that drive sports team valuations and cover some valuation concepts.

The Sports Business Model

The foundational revenue streams of a sports team are those captured inside the stadium: ticket/gate revenue, merchandise, and food and beverage. If the team or league is relevant enough, additional revenue streams include sponsorship, camps and clinics, and media rights deals. Additionally, soccer has a unique revenue stream selling or “transferring” a player to another team, often in an entirely different league, which is why teams often invest so much into their development programs.

At their core, sports teams are territory-protected intellectual property that can then be monetized in various ways. People often compare sports teams to the Disney flywheel, which uses content creation as the centerpiece that drives value to their parks, music, merchandising, and live entertainment businesses.

Once there is market validation for the sports content, owners can use it to sell tickets, merchandise, F&B, video games, highlights, etc. But the media rights are the leg of the flywheel that can make the most outsized impact on valuation.

Sports are the final frontier in live entertainment and one of the only pieces of television programming people actually sit down to watch while it’s happening in real-time. Sports represented 96-100 most-watched television programming in 2023. This makes them extremely valuable to advertisers and, in turn, to broadcasters who rely on this advertising revenue. Even tech companies with streaming products that don’t rely as heavily on advertising revenue are hungry for sports content to differentiate their platforms.

Most other revenue streams for sports teams are fixed or grow linearly. Teams can raise ticket prices and food and beverage only incrementally before destroying the delicate fan experience. Media rights packages, on the other hand, do not always grow linearly and present tremendous upside for sports teams and leagues. In a report by Rethink Research, it’s estimated that between 2014 and 2023, media rights revenues have more than doubled to $45B for the top 16 sports leagues, and project these packages will grow at a 7.25% CAGR to surpass $90B by 2033. These revenue streams have become so significant they often represent more than 50% of total league revenues.

In addition to the sheer size of the rights packages, they are often contractually guaranteed over 7-10 year periods meaning the largest revenue stream behaves similarly to SaaS revenue in a technology company.

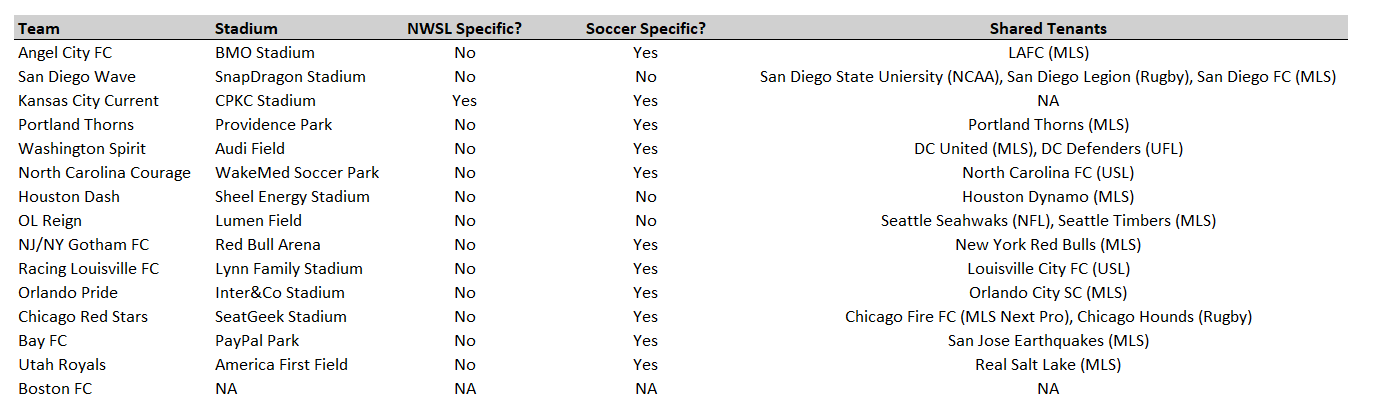

Removing media rights from the equation creates a very different business profile for a sports team and creates a neccesity to dial in the economics from all other revenue streams. Oftentimes stadium ownership is one of the clearest paths forward to do this. When owning the stadium, there is significant margin expansion on existing revenue streams (merchandise, food and beverage, parking). Additionally, the team can leverage the stadium to produce income outside the core season with concerts, community events, other sports, etc. This stadium ownership, or lack thereof, is one of the potential risks with investing in an NWSL team and makes the case study of the Kansas City Current so exciting to watch. Below is a chart that shows the current stadium ownership landscape of the NWSL.

Valuation Methodology

With the brief detour on the sports business model behind us, let's focus on valuation and return to the NWSL. In the charts I present below, along with any popular media entity that covers sports business, team valuations will almost always be presented as a multiple of revenue. Although revenue multiples are convenient and easy to understand, they are not always theoretically accurate. A business's value is not driven by how much they make but rather by how much they keep. The true intrinsic value of a company is the value of all future cash flows discounted to the present value, with cash flows represented by the cash available to providers of capital, not revenue.

Life doesn’t happen in a textbook, though, and in reality, investors use revenue multiples all the time. The most common situation that we see revenue multiples include:

The actual financial situation of a business may be unknown or information not publicly available (we can often see how much sports teams make but not necessarily how much owners keep).

The business is growing rapidly, and cash flow isn’t an accurate reflection of the company's current trajectory.

Situations where a business isn't profitable and a multiple of cash flow wouldn’t be available.

Sports teams trade on revenue multiples for all three of the above reasons. To fans and media, true financial performance is not always available but revenue can often be determined based on league sources and publically available information. Many leagues and teams are experiencing high growth, and it will take time for cash flow to reflect financial prospects. And finally, despite common perception, many sports teams aren’t profitable. Sportology Group estimates that 4-29 MLS clubs turn a profit, and most public sources estimate that no NWSL team currently turns a profit despite the nine-figure valuation.

NWSL teams trade at multiples of revenues because they are viewed similarly to a venture capital investment. An investor will pay multiples of revenue now with the expectation that the revenue growth will lead to cash flow down the road or an attractive exit opportunity to another investor willing to pay for that potential growth.

Investment Considerations

So is the NWSL a strong investment opportunity? Although this is a bit of a cop-out answer, I think there is enough data to make a strong bull case and a bear case for the NWSL. Regardless of perspective, it’s essential that an investor maintains price discipline when looking at opportunities in the NWSL. Valuation can deviate from economic principles in the near term, but over the long term, valuations must reflect the true cash-flow potential of a business.

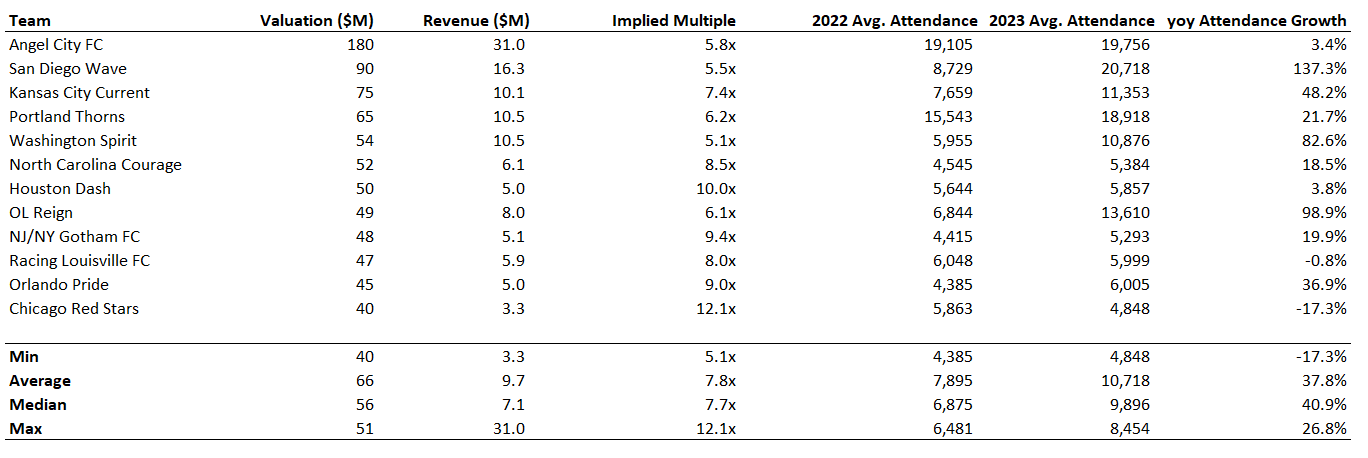

Charts 1 and 2 below show the current estimated valuations and revenues for the 12 NWSL teams that played in 2023, their attendance in 2022 and 2023, and some recent transaction data. What we see is quite a disparity in team valuations ranging from $180M for Angel FC to $40M for the Chicago Red Stars. Implied revenue multiples range from 5.1x TTM revenue to 12.1x TTM revenue.

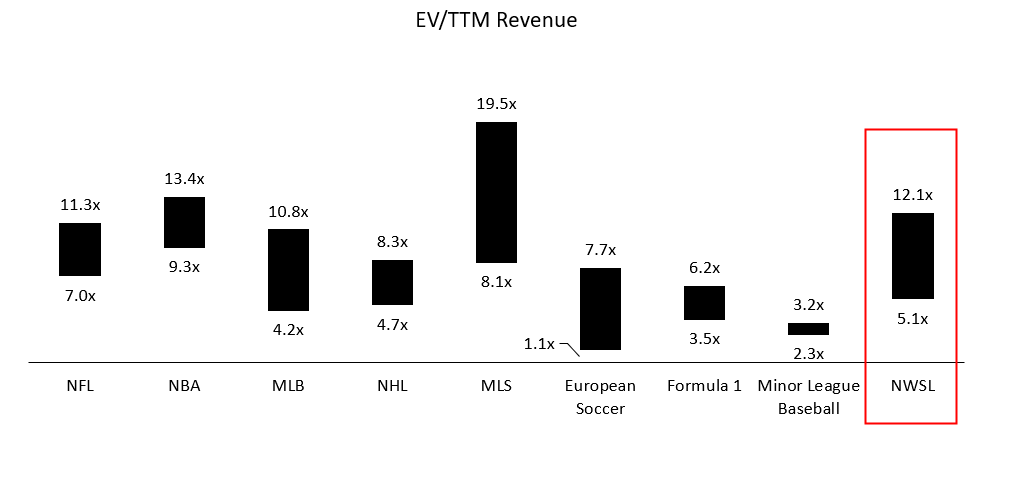

Charts 3 and 4 show how the range in revenue multiples for the NWSL compares to other major sports leagues. The average multiple paid for an NWSL team is actually larger than that paid for an MLB, NHL, F1, Premier League, and Minor League baseball team, despite a much lower revenue base. This means that investors are expecting massive growth for the NWSL from future commercialization efforts and continued step-ups in media rights deals.

Bull Case

The key elements when building out a bull case for investment in the NWSL include the potential growth in media rights, the industry tailwinds of women’s sports growth, and smart money entering with operational experience.

Although the $240M was massive compared to the previous NWSL deal, it’s a fraction of the media rights packages that more established sports entities can put together. According to Sports Media Watch, the NBA projects a potential 10-11 year, $75B deal for their next media package when their current $24B deal expires after the 2024-2025 season. The NFL recently negotiated an 11-year deal for a total payout of $113B. The $240M over 4-years means $60M per year. Given the broadcast partners are covering production costs, the 15 clubs playing in 2023 will distribute ~$60M evenly (less any team-specific production costs and the league office take). This $4M in additional revenue per team is excellent but most likely doesn’t explain the multiples new ownership groups are paying. What they are most likely baking into projections is an additional step up with the following media rights deal in 2027. With the Olympics and World Cup coming to North America shortly, expectations are that the domestic acceptance and interest in soccer will only accelerate.

Football will always be king in the US, and soccer will not replace basketball anytime soon, but looking at the media deals with these leagues along with the trajectory of women’s sports, one can build a strong bull case under the assumptions that media revenue has a lot of room to grow. The NHL recently signed a 7-year, $225M per year media rights deal with Turner Sports. Although the goals are lofty, and there is a lot more work to do, is women’s soccer catching up to professional hockey that farfetched?

We are at a significant inflection point in the growth of women’s sports. I discussed the data above, but long story short, there is an unprecedented level of talent and interest across multiple female sports properties. A vital component of the bull argument is that we are still on the ground level of women’s professional sports, and it's an ideal entry point while there is still a disparity between male and female professional sports. The upcoming women’s basketball final four may prove we are approaching parity faster than many think.

It is generally a positive signal when "smart" money, or professional, institutional investors, enter a new asset class (although this isn't always true, and this point was re-emphasized to me as I was just finishing up Michael Lewis’ “Going Infinite”). The recent turnover of NWSL owners has consisted of many families as sellers with buyer groups backed by institutional private equity. This change of hands is a positive signal because a.) these entities are return-driven, b.) they bring deep pockets to fund league and team growth, and c.) they often bring operational and commercialization expertise from similar operating companies or even existing sports franchise portfolio companies.

In November 2023, Carolyn Tisch Blodgett, CEO of Next 3 Ventures and strategic advisor to the New York Giants (NFL), joined the ownership group of the NY/NJ Gotham FC.

Sixth Street ($75B AUM) owns a majority of equity in the new expansion franchise Bay FC.

Carlyle ($426B AUM) was part of the ownership group that bought the Seattle OL Reign.

Artcos Sports Partners ($10B+ AUM) holds a minority stake in the Utah Royals.

Monarch Collective (~$100M AUM) is a women's sport-focused fund helping bring the expansion franchise to Boston.

Levine Leichtman Capital Partners ($14B AUM) led the purchase of the San Diego Wave.

Revitate, the outside investor-facing arm of the Bhathal family office, recently led the acquisition of the Portland Thorns and focuses on sports as a key vertical in addition to real estate and consumer goods.

There has been so much interest from institutional investors that in February of 2024, the NWSL leadership codified new rules to govern private equity fund’s involvement in the NWSL. The new rules prevent investment from sovereign wealth funds and state that PE funds can have passive investments in no more than three teams. Each PE fund can own 5-20% of a team's equity, with no team having more than 30% owned by multiple private equity funds.

Paring deep-pocketed operational expertise with a greenfield opportunity in the women’s sports space just scratching the surface of media rights potential leads to an investment opportunity with significant upside.

Bear Case

Many would view the relatively quick turnover of original NWSL ownership groups exiting their investment as a red flag, especially when the message is that this is just the beginning of the upside potential, and after most likely sinking large amounts of capital into the team to build out the brand, facilities, roster, etc.

The majority of the recent team transactions in the NWSL, though, were due to changing circumstances with the original owner (Seattle Reign) or pressure to sell the team from outside sources (Portland Thorns, Chicago Red Stars). What I think is more valid with a bearish perspective on the NWSL is the potential competition from other emerging leagues and the unproven nature of the demand for media rights.

Starting with competition, the NWSL is not the only professional women’s soccer league and will face competition from both the domestic USL Super League, set to debut in August of 2024, along with the European Barclays Women's Super League.

In men’s soccer, the USL Championship does not compete directly with the MLS because it’s a second-division league sanctioned by the US Soccer Federation. The USL Championship has a different talent level and focuses on smaller regional markets.

The USL Super League on the Women’s side will be different, though, as they seek top division status and a chance to compete directly with the NWSL for both player talent and consumer attention. The USL Super League will not have a salary cap, lending a deep-pocket ownership group the opportunity to poach NWSL talent, similar to what LIV Golf has been able to do with PGA Tour golfers.

The USL Super League will launch with 10-12 franchises, including Charlotte, Dallas, Lexington, Phoenix, Spokane, Tampa Bay, Tucson and Washington DC.

The Barclays Women’s Super League is the female equivalent of the Premier League in the United Kingdom. It is the top European soccer league for women and traditionally has been the landing spot for much of the US’ top female talent.

Competition aside, the more pressing concern with an investment in the NWSL is the unproven demand for the content itself or at least such a small sample size of proven traction. The NWSL is not a new league. It’s been around since 2012 without much media attention. This most recent media rights deal has driven the recent valuation growth in franchises. With this current deal only lasting four years, people will quickly know whether or not the present valuations are sustainable. If there is traction with consumer interest, streamers and traditional broadcasters will bid up the price of the next package due in 2027. If there is little evidence to justify the spending, the NWSL may face a flat or, worse yet, smaller media rights package that will cause team valuations to come crashing down. With little data to prove there is demand for NWSL content over the long term, I think the strongest bear argument would be that teams are being valued based on future media rights deals that are far from guaranteed. If you take the media rights deals out of the equation, very few teams have a business model or stadium ownership that can support an enduring sports franchise, let alone one at a nine-figure valuation.

If future media rights packages don’t materialize, the NWSL faces a very different outlook. In that case, teams must generate returns from the traditional stadium-centric revenue streams. Minor league baseball teams, which generally trade 2-4x revenue become a more relevant comp. Revenue growth is capped by limited media rights interest and a localized fanbase. Despite a smaller revenue base, minor league baseball can still be an attractive investment target, albeit offering a very different return profile with a distinct business model. On the revenue side, they put people in seats by emphasizing the value of entertainment alongside the sporting event itself (the Savanah Bananas have taken his notion successfully to the extreme). On the cost side, minor league baseball teams are often able to turn a profit primarily because the major league affiliates subsidize most of the minor league team's player salaries.

I’m not saying that minor league baseball is a relevant comp at the present moment. The NWSL is the top-tier women’s professional soccer league in the world, while the minor league is a development league for the top-tier MLB. There is substantially more upside potential with the NWSL compared to MiLB. However, a bear case for the NWSL would propose that the current valuations of clubs do not accurately reflect the expected value of landing that next big media deal.

Conclusion

Beyond the investment considerations, I do believe that the capital being deployed into the NWSL is extremely important for the growth of women’s professional soccer and the broader objective of closing the gap in pay between men’s and women's professional athletes. These are the ancillary considerations that won’t necessarily show up on an income statement but are equally, if not more, important.

With that being said, I personally lean more towards the bull case presented above and believe that women’s professional soccer and the NWSL is not an ephemeral trend but rather a legitimate piece of sports IP with tremendous upside potential. The multiples being paid now reflect the future prospects of the league and the growth that will continue to materialize in the form of media contracts, venues built specifically for the sport, and expansion of the salary cap. This first year of the new media deal will be incredibly important, and I’m personally excited to see a whole lot more. I’m hoping for an expansion franchise in my home base of Austin, Texas, in the near future!